CRED IQ Defeasance Trends…

As the commercial real estate industry continues to adjust to a rising interest rate environment, CRED iQ examined the latest trends in defeasance activity. Reports of defeasance requests have trended higher in recent months. Generally, in a low-rate environment defeasance is an opportunity for borrowers to take advantage of refinancing existing debt at a comparatively lower rate. In the current environment of rising interest rates, borrowers are motivated by risk from the opportunity cost of waiting to refinance at maturity when rates could be significantly higher than current rates or the risk of not cashing out equity before a recessionary environment could adversely impact commercial real estate values.

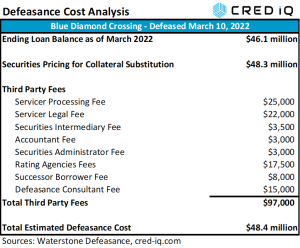

Other factors to consider are rising US treasury yields compared to 2021. With higher US treasury yields, substituting real estate collateral for US treasuries or similar securities that match loan cash flows becomes more economical from a cost perspective. In addition to the cost of purchasing cash-flow-equivalent securities, defeasance costs also comprise additional fees which generally can include accounting fees, consulting fees, costs associated with a legal review or rating agency confirmation, custodial fees for the collateral securities, servicer processing costs, and costs associated with the successor borrower. As an example, Blue Diamond Crossing is a $46 million loan that defeased on February 10, 2022. The loan will be open for prepayment in December 2022 and has a maturity date of April 1, 2023, which was more than a year from the time of defeasance. The event was driven by the borrower securing a new refinancing package for the loan collateral, a 505,072-sf retail center in Las Vegas, NV. The borrower was able to take advantage of a lower cost of capital compared to loan origination in 2013 while also staying ahead of imminently higher interest rates. The total cost of defeasance was more than $48 million, approximately 5% higher than the outstanding balance of the loan at the time. The defeasance cost analysis for this particular transaction is detailed in the table below.

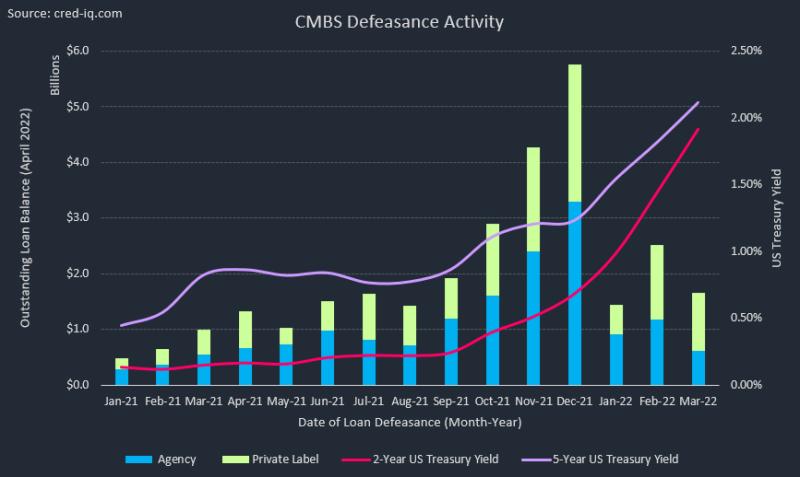

Overall, CRED iQ identified more than 6,000 loans — across CMBS conduit, SBLL, CRE CLO and Freddie K securitizations — with an outstanding balance greater than $65 billion that were defeased as of March 2022. Defeasance activity during Q1 2022 totaled $5.6 billion across more than 350 loans. For each month in Q1 2022, defeasance activity was higher year over year than in 2021. The largest difference was in February 2022, when defeasance activity was nearly 4x higher than the February 2021 total, based on outstanding balance. Most recently in March 2022, the average time to maturity for loans that defeased was approximately 3.5 years. Extending the view historically, time to maturity generally averaged from three to four years for loans that defeased during 2021 and through Q1 2022.

Multifamily was the property type most commonly associated with defeasance by a wide margin, accounting for greater than 60% of all properties that were substituted. However, this figure was inclusive of Freddie K securitizations. Isolating defeasance activity to conduit and SBLL transactions (CRE CLO defeasance was nominal), multifamily was still the property type most commonly associated with defeasance with 25% of activity by outstanding balance. Office was close behind, accounting for 24% of outstanding defeased loans by unpaid balance. Unsurprisingly, loans secured by lodging collateral were least commonly defeased given headwinds faced by the industry during the pandemic. Loans previously secured by lodging collateral accounted for 5% of all defeased loans

Recent observations of client defeasance calculator usage (integrated and powered by Waterstone Defeasance) show a surge in activity. The increase in defeasance appetite across CRED iQ users is expected to remain elevated over the near to intermediate term. According to George Rodriguez, principal at Waterstone Defeasance:

“Defeasance activity continues to spike up due to the Fed taking action to combat inflation, with rate increases of 75 bps and another 100 bps or more waiting in the wings over the next two quarters. Borrowers are now actively reviewing their exit strategies, selling or refinancing to extract the equity in their real estate holdings as well as locking in current rates now vs refinancing at a higher rate as they near their loan maturities.

Defeasance advisors and servicers are having a busy spring and we are forecasting more of the same through the summer. Where the Fed lands over the next several months on rate hikes to battle inflation, may start to impact real estate valuations and higher cap rates. We are starting to see the lenders tapping their breaks on securitizations as the Fed tries for a soft landing as bond buyers watch cautiously.”

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Agency loan and property data.