With over 100 years of combined experience, our advisors understand the defeasance process from the inside out. We help property owners and brokers navigate the intricacies of commercial real estate loan exiting.

After defying recession fears this year, the US economy is forecast by Goldman Sachs Research to beat consensus expectations in 2024. US GDP is projected to expand 2.1% in 2024 on a full-year basis, Goldman reaffirmed its longstanding view that the probability of a US recession is at just 15% over the next 12 months.

As inflation continues its moderating trajectory over the coming quarters, JP Morgan thinks it is likely the FOMC will start to slowly normalize policy rates later in 2024. Further, it is their belief, a forecast 50 bps of cuts in both 3Q24 and 4Q24, bringing the Fed Funds target range to 4.25%-4.50% by the end of 2024.

The US inflation rate is seen easing closer to the Federal Reserve’s 2% target next year in the latest forecast from the Congressional Budget Office, as economic growth and labor market activity cools.

Trends:

Resilient labor markets, in combination with expensive single-family mortgages, are helping to maintain robust demand for multifamily. The past three months has seen demand for apartments grow to 89,280 units, 11% higher than the prior three months and more than six times above last year’s mark of roughly 13,000 units. This is according to Cushman & Wakefield.

The U.S. retail real estate market remained strong in the past three months of 2023, thanks to healthy tenant demand and resilient consumer spending. The vacancy rate came in at a historic low of 5.4%, down 5 basis points (bps) from the prior three month level, also according to Cushman.

Industrial fundamentals showed increasing signs of slowing in the past three months as the turbulent macroeconomic environment persists. With decreased leasing velocity and sluggish pre-leasing rates, absorption figures continued to slow, per JLL.

Defeasance Market:

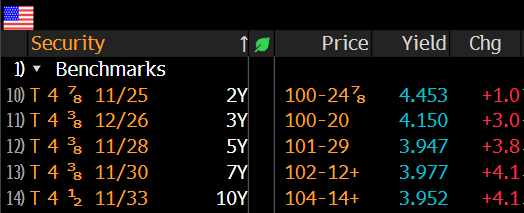

The cost of defeasance continues to be relatively low, because of higher rates and the inverted yield curve.

Although the number of transactions for 2023 is lower than 2024, deals are still getting done, driven by sales and refinancing is selective situations and asset classes. These include Self-Storage, Retail, Multifamily and NNN.