With over 100 years of combined experience, our advisors understand the defeasance process from the inside out. We help property owners and brokers navigate the intricacies of commercial real estate loan exiting.

A broad slowdown in inflation continued in October, this may end likely the Federal Reserve’s interest-rate increases. This according to the Wall Street Journal.

Consumer prices overall were flat last month and rose 3.2% from a year earlier, a slower pace than in September as prices for gasoline fell, the Labor Department reported.

Core inflation for the five months ended in October was at a 2.8% annual rate. Overall inflation hit a recent peak of 9.1% in June 2022.

“The 12-month inflation rate is on track this year to have posted its largest slowdown in at least four decades” said Chicago Fed President Austan Goolsbee.

Trends:

The estimate of Q3 GDP shows the U.S. economy likely grew at an annualized rate of 4.9%, the fastest pace in almost two years, reaffirming the strength of the U.S. economy and its consumers despite tighter monetary policy and price pressures. This after 2.1% annualized growth in Q2, and 2.2% in Q1 (revised). Per Cushman and Wakefield.

Commercial Real Estate fundamentals are softer but it’s more so the cost of debt that’s limiting transaction volume. Dramatically higher base rates and drifting spreads have pushed best fixed interest rates to 6.50- 6.75% and best floating rates 7.25-7.50% which is pressuring cap rates and values, and in some cases causing a bid-ask spread between sellers and buyers trying to avoid negative leverage. The lack of demand for debt has impacted placement volumes significantly below the 2021 and 2022 peaks—the result of fewer trades and no elective refinancings. Also according to C&W.

Distress exists but activity has been muted so far, limited to office assets and situational cap stack distress in other asset classes (like multifamily) driven by higher interest rates. Distress typically lags the market, but time will bring more opportunities as in-the-money rate caps expire, and a wave of 2024-2025 maturities increase the need for rescue capital.

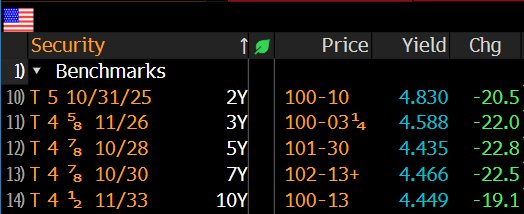

Defeasance Market:

The cost of defeasance continues to be relatively low, because of higher rates and the inverted yield curve the defeasance “premiums” are actually negative in many cases.

Transactions getting done across the country continue to be driven by mostly select property types; Self-Storage, Retail, and NNN.