Economic Climate:

Growth: The U.S. economy is expected to continue expanding at a slower pace through 2026 as elevated interest rates, tighter credit conditions, and softer business investment weigh on overall activity, though resilient consumer spending has so far helped avoid a sharp downturn. Recent estimates place 2026 U.S. GDP growth between approximately 1.5% and 2.0%, down from stronger post-pandemic expansion levels seen in prior years.

Inflation: Inflation is projected to gradually ease but remain above the Federal Reserve’s 2% target for much of the year, with housing, insurance, healthcare, and wage-related costs continuing to keep price pressures elevated across the economy. Core CPI inflation (which excludes food and energy) was up 0.38% month-over-month and 2.75% year-over-year for April. With conflicts still ongoing in the Middle East, inflation remains persistent which could delay potential rate cuts for 2026.

Labor Market: The labor market is expected to cool moderately rather than contract significantly, with slower hiring, modest increases in unemployment, and easing wage growth helping reduce inflationary pressure while still supporting overall economic stability. The unemployment rate has remained near historically low levels around 4.1%–4.3%, while monthly payroll growth has averaged roughly 140,000–175,000 jobs in recent months.

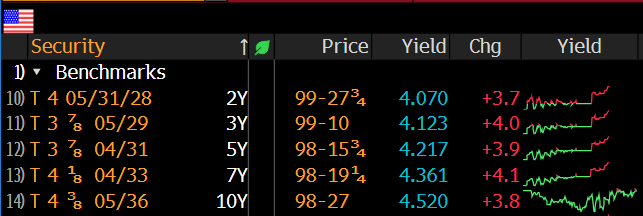

Federal Reserve Outlook: The Federal Reserve is expected to maintain a cautious policy stance in 2026, with markets anticipating limited and gradual rate cuts as policymakers continue balancing slowing economic growth against still-persistent inflation risks. The federal funds rate currently remains in the 4.25%–4.50% range, while 10-year Treasury yields have recently fluctuated between approximately 4.4% and 4.7% amid shifting rate-cut expectations.

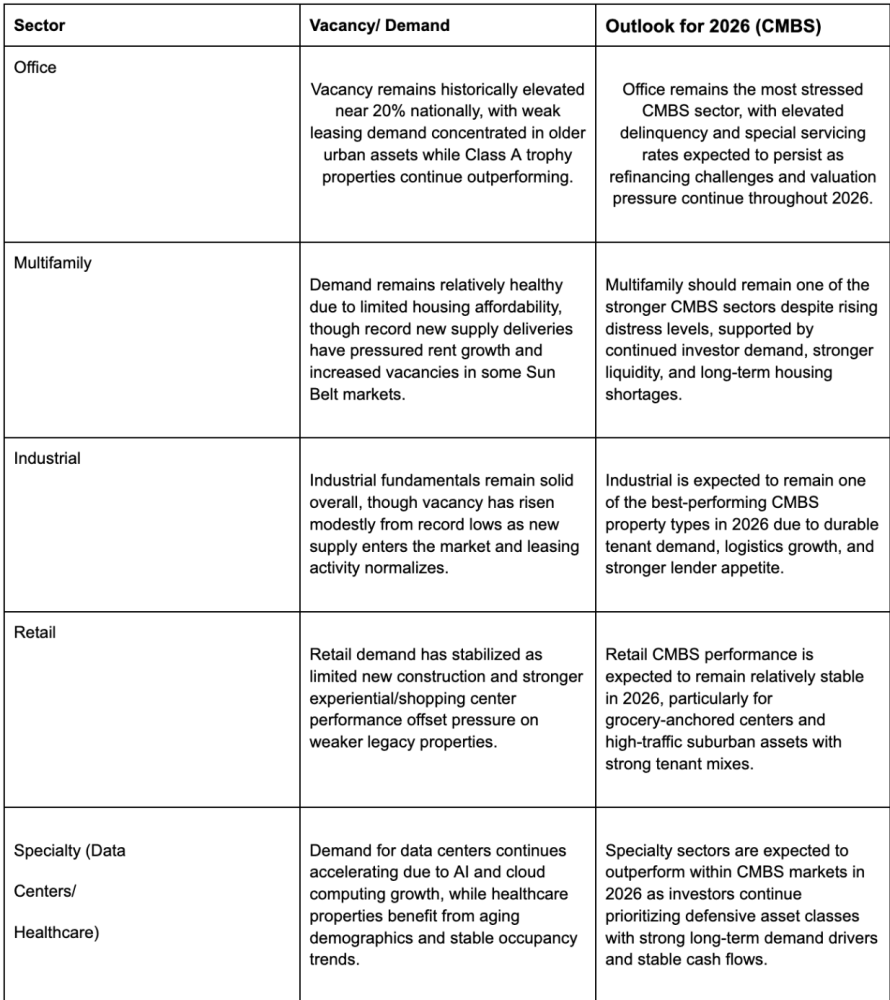

Commercial Real Estate outlook:

Fundamentals: Commercial real estate fundamentals are expected to remain mixed across property types in 2026, with industrial, data center, and select multifamily assets continuing to outperform while office properties face ongoing vacancy and leasing pressure. Office vacancy rates nationally remain near record highs around 20%, while multifamily rent growth has stabilized in the low single digits following significant supply deliveries over the past two years.

Capital Markets: CRE capital markets activity is expected to improve gradually as transaction volumes recover from depressed 2023–2025 levels and investors adjust to the higher-rate environment. CMBS issuance has rebounded significantly, with 2025 issuance surpassing $125 billion and early 2026 volumes continuing to trend higher as lenders regain confidence and spreads stabilize.

Debt and Distress: Refinancing pressure will remain one of the largest challenges facing commercial real estate as a substantial volume of loans mature into materially higher interest rates and lower property valuations. Industry estimates indicate more than $500 billion of CRE debt is scheduled to mature in 2026, while CMBS delinquency rates have climbed above 7% and office delinquencies remain above 11%.

Outlook: The broader CRE outlook for 2026 is cautiously improving but remains highly dependent on interest rates, Treasury volatility, and lender liquidity. If inflation continues moderating and the Federal Reserve begins gradual rate cuts later in the year, transaction activity, refinancing volume, and defeasance activity could accelerate meaningfully during the second half of 2026.