Economic Climate:

Growth: U.S. economy is slowing but still expanding (~2%), with softer Q1 momentum driven by weaker consumption and external shocks. High-frequency data (retail sales, ISM) suggest demand is cooling, but resilient household balance sheets and services activity are preventing a sharper downturn.

Inflation: Disinflation has stalled; core inflation is running ~2.7% with upside pressure from energy and tariffs. The latest PPI reading for February 2026 showed a 3.4% YoY rise, with core producer inflation up around 3.9% annually. Recent increases in oil prices and supply-side frictions are feeding into core components, raising concern that inflation could remain above the Fed’s 2% target longer than expected.

Labor Market: Conditions remain stable but are cooling—unemployment is drifting toward ~4.4% with subdued hiring activity. The market is characterized by slower job creation and declining job openings rather than layoffs, indicating a gradual rebalancing rather than a sharp deterioration.

Federal Reserve: Rates are on hold (~3.5–3.75%); the Fed remains cautious with limited room to cut amid sticky inflation. Policymakers are balancing the risk of easing too soon against the risk of overtightening, with current policy remaining modestly restrictive to contain inflation. Jerome Powell emphasized a data-dependent, cautious stance in March, signaling the Fed is willing to hold rates higher for longer until inflation shows clearer progress. His messaging reinforced that rate cuts are not imminent and will depend on sustained evidence of disinflation, particularly in core services and wage growth.

Risk Outlook: Rising stagflation risk as higher oil prices, geopolitical tensions, and trade policy pressure growth and inflation simultaneously. If energy prices remain elevated while growth continues to slow, the Fed could face a more difficult policy tradeoff between supporting the economy and controlling inflation.

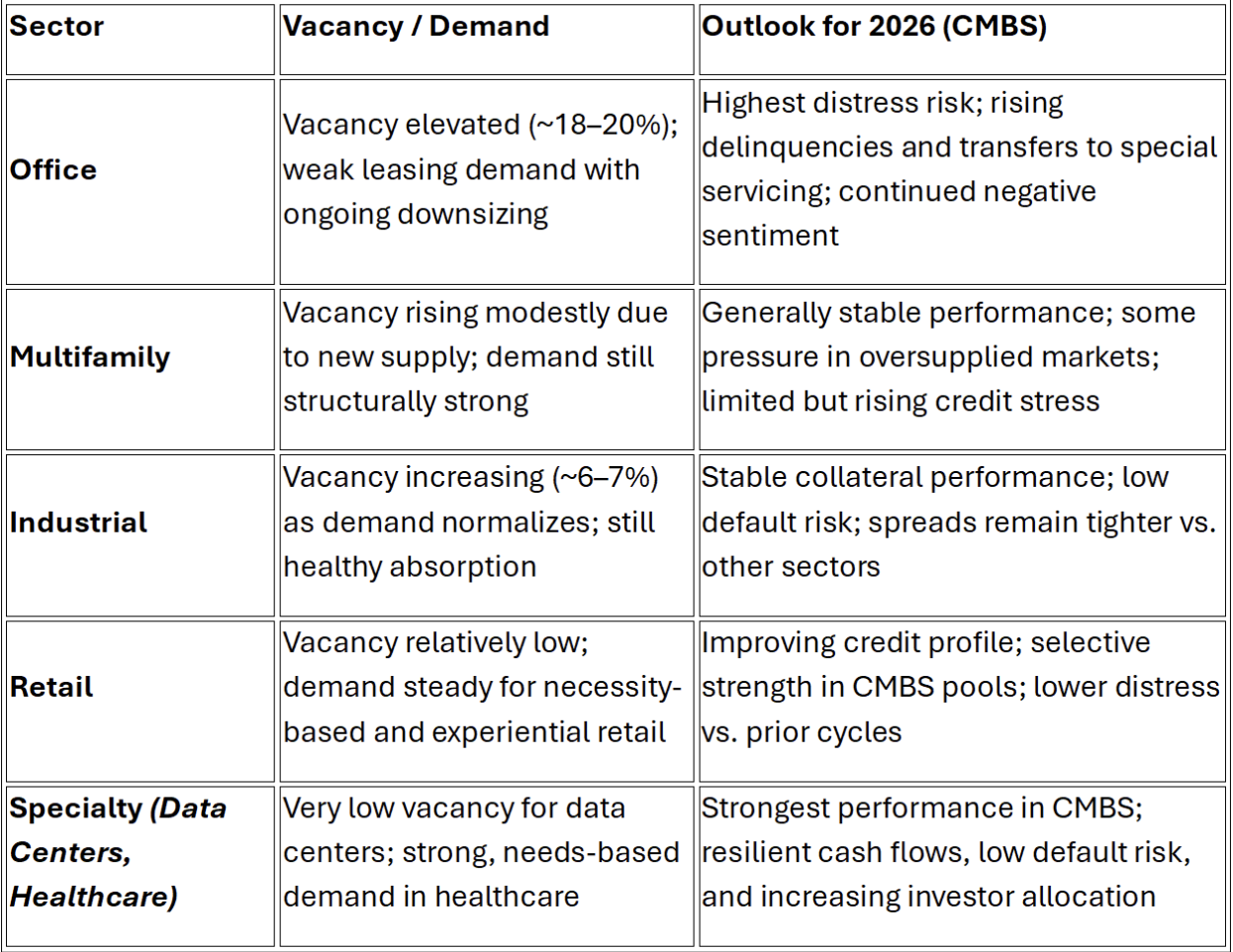

Commercial Real Estate outlook:

Fundamentals: CRE performance remains uneven across sectors. Office continues to struggle with high vacancy and weak demand, while multifamily, industrial, and retail are stabilizing with more balanced supply-demand dynamics.

Capital Markets: Investment activity is still muted due to elevated interest rates and pricing uncertainty. Bid-ask spreads persist, though gradual price discovery and modest cap rate expansion are helping transactions slowly recover.

Debt & Distress: Refinancing pressure is building as loans hit maturity in a higher-rate environment. Office remains the primary source of distress, with rising delinquencies, extensions, and restructuring activity across lenders.

Outlook: The sector is undergoing a gradual reset rather than a sharp correction. Performance will remain mixed, with high-quality assets outperforming while challenged properties face continued valuation and liquidity pressure through 2026.