With over 100 years of combined experience, our advisors understand the defeasance process from the inside out. We help property owners and brokers navigate the intricacies of commercial real estate loan exiting.

According to Vanguard, the U.S. economy has regained momentum after the end of the 43-day federal shutdown — they lift their 2025 growth estimate to about 1.9%.

Third-quarter 2025 data suggests growth remained solid: private business investment and consumer demand held up relatively well, and many states saw income growth.

Inflation has moderated somewhat (though still elevated compared with long-term targets): the preferred inflation metric for the central bank — core PCE — is modestly below the headline CPI.

Some analysts expect that after a likely Q4 drag due largely to the government shutdown, the economy could rebound in early 2026 — potentially aided by stabilized data flows and what could be interest-rate cuts by the Federal Reserve (Fed) in the first half of 2026.

On balance, many economists currently see the odds of a full-blown recession over the next 12 months as moderate (not high)

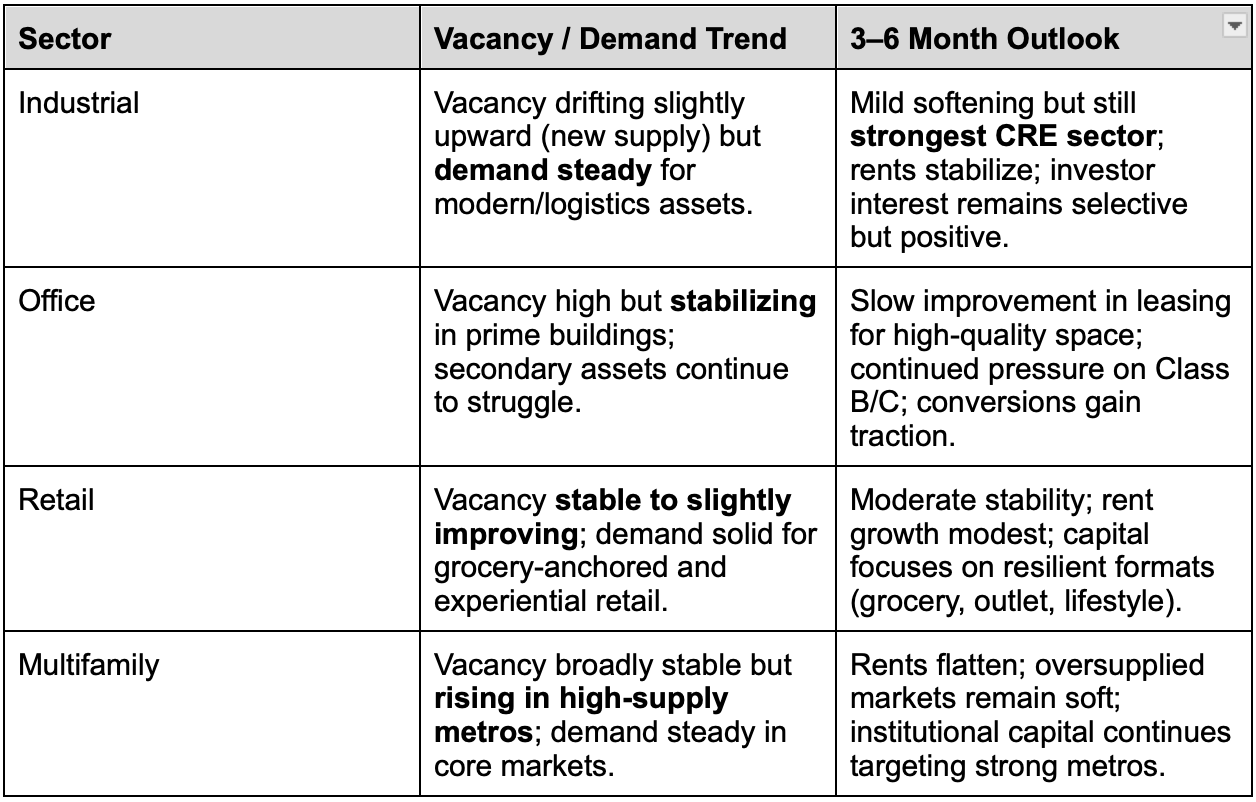

Commercial Real Estate Outlook:

Lending activity has picked up again: in Q3 2025, CRE lending accelerated as interest-rate conditions stabilized and credit spreads narrowed—helping revive deal flow across property types.

Investor confidence and capital-market activity are rising. According to a recent global index of real-estate capital markets, “bidder competitiveness” increased in October, consistent with growing liquidity and renewed interest in CRE investments.

However, gains are inconsistent: across the broader CRE market, fundamentals remain uneven — some sectors (industrial, well-located small-scale assets) outperform, while others (older office buildings, non-core retail) still struggle.

Defeasance update:

With a large “maturity wall” of CRE loans — a substantial share of roughly $4.8 trillion total CRE debt remains outstanding, and many loans are coming due through 2026 — defeasance is becoming a more likely exit path for borrowers facing refinancing pressure.

Given still-elevated interest rates and Treasury yields, replacing loan collateral with Treasuries (the defeasance route) is relatively more attractive — the cost of building the replacement-security portfolio is lower than in prior low-rate periods.

Overall, the outlook points to a steady uptick in defeasance volume over the next 12–18 months, influenced by interest-rate movements, Treasury yields, and sector-specific fundamentals.