With over 100 years of combined experience, our advisors understand the defeasance process from the inside out. We help property owners and brokers navigate the intricacies of commercial real estate loan exiting.

August’s economic landscape is marked by pervasive caution. In the U.S., growth is tentative but showing signs of turnaround, and central banks are signaling potential easing.

Second-quarter GDP posted a modest rebound (~ 3 % annual rate) after a contraction in Q1, though growth remains sluggish (~1.2 % for H1).

However, the biggest news for the economy came from Jackson Hole on August 22, as Chair Powell opened the door to interest-rate reductions—possibly as early as September—citing cooling labor markets and easing inflation, despite inflation still exceeding the 2 % target (~ 2.7 %).

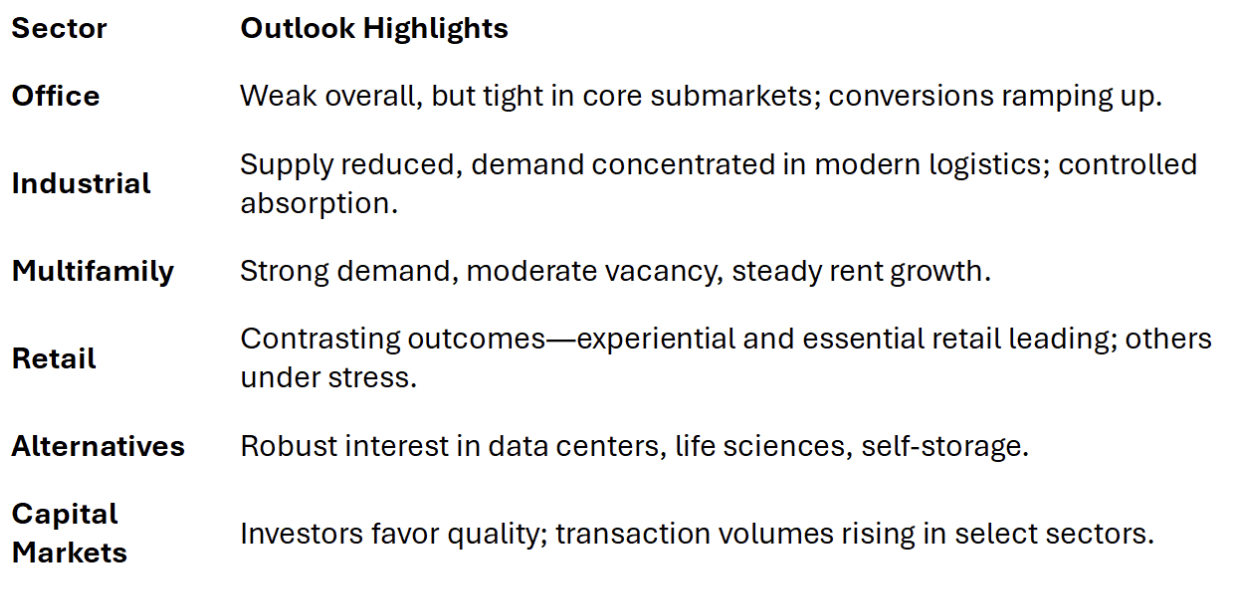

Commercial Real Estate outlook:

Q3 2025 reflects a cautiously optimistic commercial real estate market, especially compared to the more restrained environment in Q3 2024. Key indicators—availability rates, leasing volumes, and transaction activity—are showing tangible improvements.

A 2025 Deloitte survey showed a dramatic shift in sentiment: 68% of respondents now expect CRE fundamentals—including cost of capital, leasing, and prices—to improve, compared to just 27% a year earlier.

Defeasance update:

Demand for premium, well-located assets strengthened in 2025. For instance, New York City raised $11 billion in CMBS office lending—its highest total since 2021—and Midtown availability dropped from 18.2% to 15.5% year-over-year

With the Fed signaling rate cuts as early as September, more borrowers will look to defease high-coupon CMBS loans to refinance at lower rates.

Expect steady growth in defeasance volumes in Q3–Q4 2025, concentrated in loans with strong collateral (multifamily, industrial) and in markets with rising liquidity, but not yet a full return to 2018–2019 highs.