With over 100 years of combined experience, our advisors understand the defeasance process from the inside out. We help property owners and brokers navigate the intricacies of commercial real estate loan exiting.

Latest estimates show U.S. GDP growth slowed sharply at the end of 2025, expanded at a modest pace overall (about +2.2%for the year) after strong mid-year growth was weighed down by a prolonged government shutdown.

Some projections for 2026 show growth around~1.8%–2.4% — moderate rather than robust.

Inflation is elevated but easing

Inflation, though down from pandemic-era peaks, remains above the Federal Reserve’s 2% target, likely in the ~2.4–3% range through 2026.

Price pressures have been sustained partly by tariffs and higher import costs, but core services inflation is gradually moderating.

Labor market is cooling but not weak

Unemployment has ticked up from historic lows to around 4.3%, signaling some softening in hiring, but joblessness remains relatively low.

Wage growth has slowed from its rapid pace, and hiring has become more cautious.

Monetary policy remains cautious

The Federal Reserve has been holding interest rates in a higher range (~3.75%) and markets expect possible rate cuts later in 2026 if inflation continues to soften.

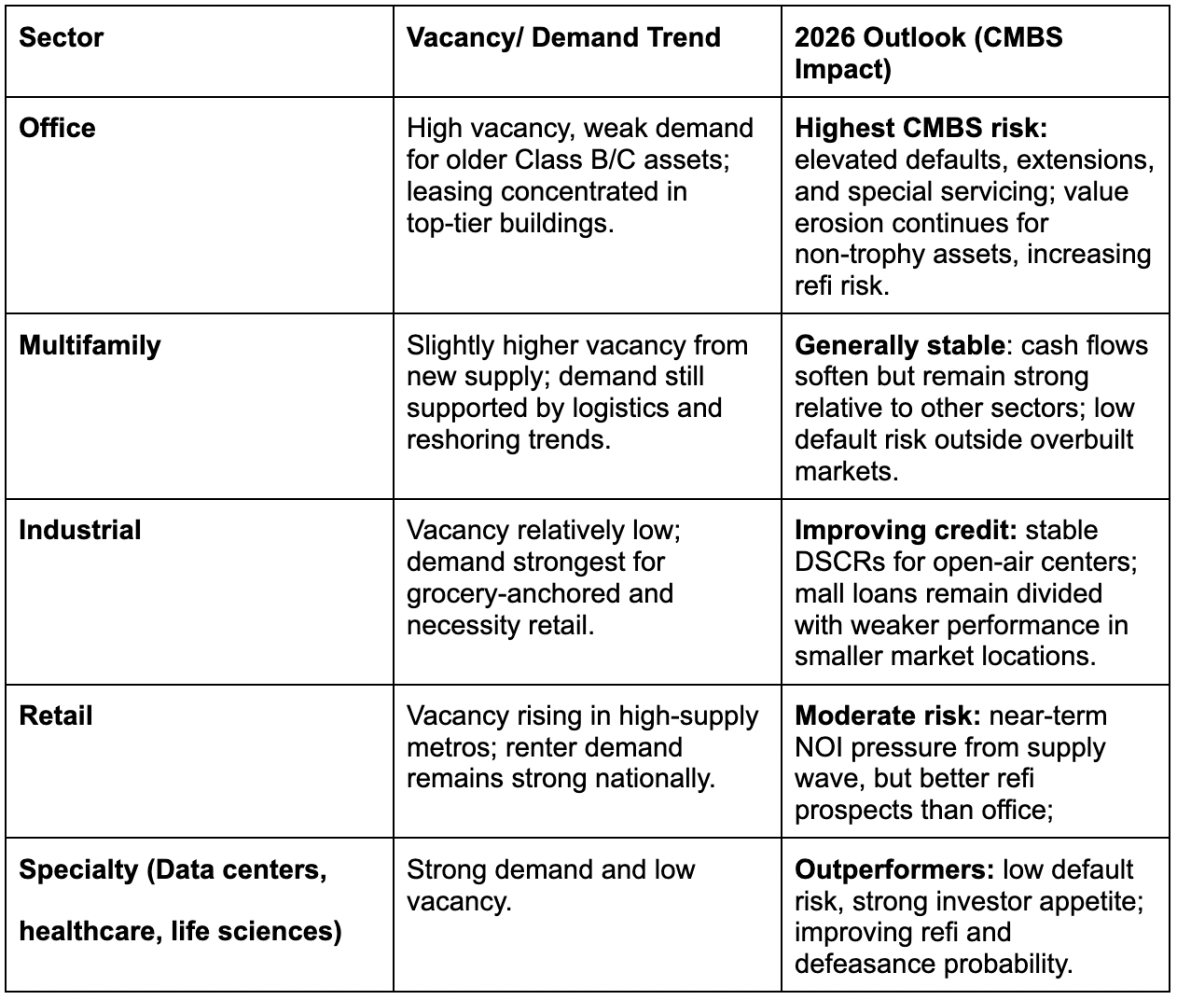

Commercial Real Estate outlook:

Stabilization, not a boom: U.S. commercial real estate is moving from correction toward stabilization; leasing and transactions are picking up slowly, but recovery is uneven by property type.

Sector split: Office remains weak (especially older buildings) with a continued flight to quality; industrial is cooling slightly due to new supply; retail and multifamily are relatively steady.

Capital markets improving: Lenders and investors are becoming more active as pricing resets and rate expectations improve, but deals are still selective and conservative.

Key risks: Interest-rate volatility and broader economic slowdown could delay recovery, especially for highly leveraged or low-quality assets.

Defeasance update:

Activity increases modestly: Defeasance volume is expected to rise versus 2025 as more loans hit maturity and borrowers seek flexibility to sell or refinance, but higher-for-longer rates keep activity below pre-2022 norms.

Volumes edging higher: Defeasance activity is up modestly versus last year as more CMBS loans reach maturity and property sales pick up but remains well below pre-2022 levels.

Sales-driven, not refi-driven: Most defeasance is tied to asset dispositions (industrial, retail, specialty) rather than traditional refinancing due to still-tight credit and valuation gaps.

Rates are the swing factor: Treasury yield declines would meaningfully improve defeasance economics and trigger higher volume; stable or higher yields keep transactions selective.

Expect gradual growth in defeasance through 2026, with activity concentrated in high-quality assets and motivated sellers rather than broad-based prepayment waves.